AML/CFT Supervisors in Puerto Rico

Puerto Rico is an unincorporated territory of the United States. Therefore most U.S. federal laws apply to Puerto Rico and the U.S. is responsible for monitoring and regulating Anti Money Laundering (AML) activities in Puerto Rico.

The Financial Crimes Enforcement Network (FinCEN) is the primary AML/CFT regulator in the United States and Puerto Rico. FinCEN is a bureau of the U.S. Department of the Treasury. FinCEN’s mission is to safeguard the financial system from illicit use and combat money laundering and to promote national security through the collection, analysis, and dissemination of financial intelligence and strategic use of financial authorities. FinCEN carries out its mission by receiving and maintaining financial transactions data; analyzing and disseminating data for law enforcement purposes; and building global cooperation with counterpart organisations in other countries and with international bodies.

How to comply with AML/CTF regulations in Puerto Rico?

As mentioned above, Puerto Rico is bound by U.S. federal laws. The Bank Secrecy Act and the Patriot Act are the two main AML Regulations.

Bank Secrecy Act: The BSA is the nation's first and most comprehensive Federal anti-money laundering and counter-terrorism financing (AML/CFT) statute. The BSA authorizes the Secretary of the Treasury to issue regulations requiring banks and other financial institutions to take precautions against financial crime, including the establishment of AML programs with the appropriate customer due diligence (CDD), screening measures and the filing of reports and record-keeping. These measures have been highly useful in criminal, tax, and regulatory investigations and proceedings, and in certain intelligence and counter-terrorism matters.

Patriot Act: "Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism (USA PATRIOT) was passed in 2001 under the context of September 11 terrorist attacks. The purpose of the USA PATRIOT Act is to deter and punish terrorist acts in the United States and around the world, and to enhance law enforcement investigatory tools, amongst other purposes. This legislation expands the scope of BSA and gives law enforcements agencies the following additional surveillance powers:

Allows law enforcement to use surveillance against more crimes of terror

Allows federal agents to follow sophisticated terrorists trained to evade detection

Allows law enforcement to conduct investigations without tipping off terrorists

Allows federal agents to ask a court for an order to obtain business records in national security terrorism cases

The Patriot Act facilitated information sharing and cooperation among government agencies so that they can better "connect the dots”.

The Patriot Act updated the law to reflect new technologies and new threats.

The Patriot Act increased the penalties for those who commit terrorist crimes

How to comply with BSA and USA Patriot Act?

Under the Bank Secrecy Act (BSA) and related anti-money laundering laws, banks must:

- Establish effective BSA compliance programs which should include to, provide for a system of internal controls to assure ongoing compliance; provide for independent testing for compliance; designate an individual responsible for coordinating and monitoring day-to-day compliance; and provide training for appropriate personnel.

- Establish effective customer due diligence systems and monitoring programs

- Screen against Office of Foreign Assets Control (OFAC) and other government lists

- Establish an effective suspicious activity monitoring and reporting process

- Screen against Office of Foreign Assets Control (OFAC) and other government lists

- Develop risk-based anti-money laundering programs

- Develop Customer Due Diligence (CDD) Programs

- Develop Customer Identification Program (CIP)

- Keep records of cash purchases of negotiable instruments,

- File reports of cash transactions exceeding $10,000 (daily aggregate amount), and

- Report suspicious activity that might signal criminal activity (e.g., money laundering, tax evasion)

How to comply with BSA and USA Patriot Act?

Under the Bank Secrecy Act (BSA) and related anti-money laundering laws, banks must:

- Establish effective BSA compliance programs which should include to, provide for a system of internal controls to assure ongoing compliance; provide for independent testing for compliance; designate an individual responsible for coordinating and monitoring day-to-day compliance; and provide training for appropriate personnel.

- Establish effective customer due diligence systems and monitoring programs

- Screen against Office of Foreign Assets Control (OFAC) and other government lists

- Establish an effective suspicious activity monitoring and reporting process

- Screen against Office of Foreign Assets Control (OFAC) and other government lists

- Develop risk-based anti-money laundering programs

- Develop Customer Due Diligence (CDD) Programs

- Develop Customer Identification Program (CIP)

- Keep records of cash purchases of negotiable instruments,

- File reports of cash transactions exceeding $10,000 (daily aggregate amount), and

- Report suspicious activity that might signal criminal activity (e.g., money laundering, tax evasion)

What are my AML/CTF reporting obligations?

Under the Bank Secrecy Act (BSA) and related anti-money laundering laws, banks must:

- Currency transaction reports (CTR): Reports cash transactions exceeding $10,000 in one business day, regardless of whether it's in one transaction or several cash transactions. It is filed electronically with the Financial Crimes Enforcement Network (FinCEN) and is identified as FinCEN Form 112 (formerly Form 104). Certain fields in the CTR are marked as “critical” for technical filing purposes. This means the BSA E-Filing System does not accept filings in which these fields are left blank. FinCEN expects that banks will provide the most complete filing information available, consistent with existing regulatory expectations, regardless of whether the individual fields are deemed critical for technical filing purposes. If the bank receives correspondence from FinCEN identifying data quality errors, it should follow any required actions that FinCEN outlines in the correspondence. A completed CTR must be electronically filed with FinCEN within 15 calendar days after the date of the transaction. The bank must retain copies of CTRs for five years from the date of the report. The bank may retain copies in either electronic format or paper copies.

- Suspicious activity report: A suspicious activity report (SAR) must report any cash transaction where the customer seems to be trying to avoid BSA reporting requirements by not filing CTR or monetary instrument log (MIL). A SAR must also be filed if the customer's actions suggest that they are laundering money or otherwise violating federal criminal laws and committing wire transfer fraud, check fraud, or mysterious disappearances. These reports are filed with FinCEN and are identified as Treasury Department Form 90-22.47 and OCC Form 8010-9, 8010-1. A financial institution is required to file a suspicious activity report no later than 30 days after the date of initial detection of facts that may constitute a basis for filing a suspicious activity report. If no suspect was identified on the date of detection of the incident, a financial institution may delay filing a suspicious activity report for an additional 30 calendar days to identify a suspect. In no case shall reporting be delayed more than 60 calendar days after the date of initial detection of a reportable transaction. A financial institution is not allowed to inform a business or consumer that a SAR is being filed, and all the reports mandated by the BSA are exempt from disclosure under the Freedom of Information Act.

- Cash Purchases of $3,000-$10,000, Inclusive: MSBs that sell money orders or travellers’ checks are required to record cash purchases involving $3,000-$10,000, inclusive. Multiple cash purchases of monetary instruments totalling $3,000 or more must be treated as one purchase which must be recorded if they are made at the same time, or the MSB has knowledge that such purchases occurred during one business day.

- Money Transfers of $3,000 or More: MSBs that provide money transfer services must obtain and record specific information for each money transfer of $3,000 or more, regardless of the method of payment. MSBs must keep the record for 5 years from the date of the transaction.

- Currency Exchanges of More Than $1,000: Currency exchangers must keep a record of each exchange totalling more than $1,000 in either domestic or foreign currency, and keep the record for 5 years from the date of transaction.

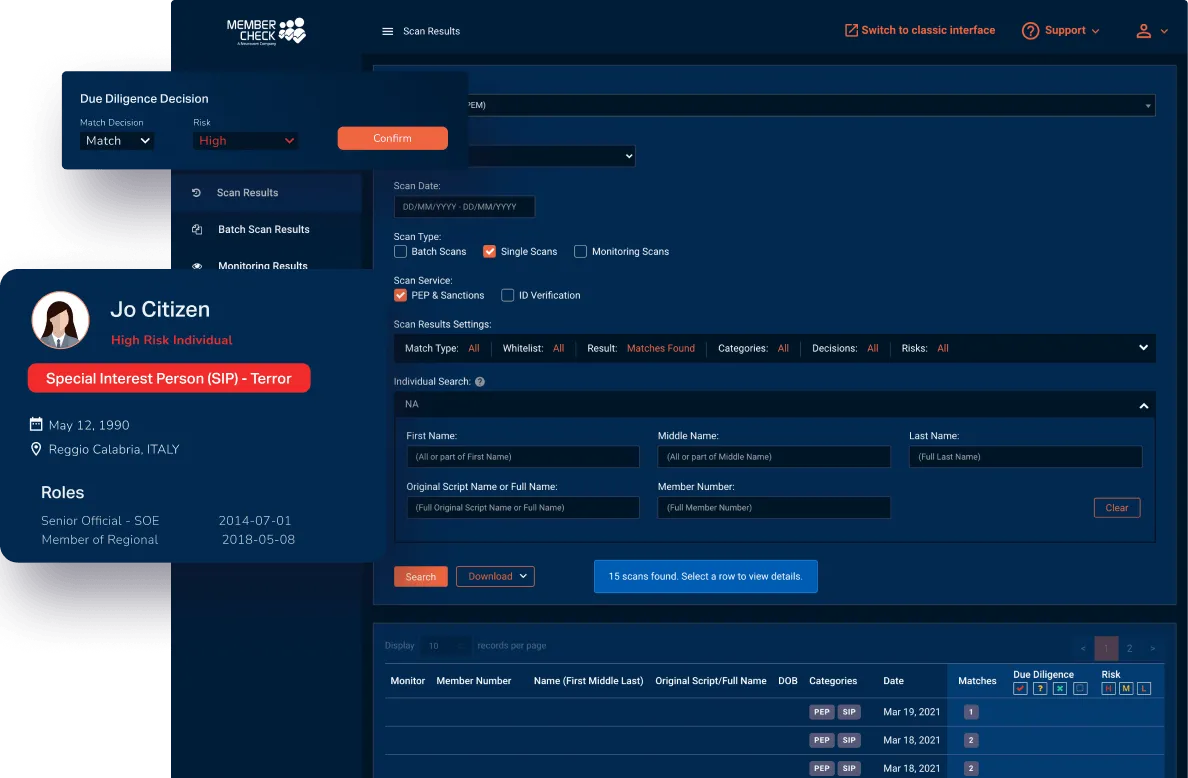

How can MemberCheck Help?

Our clients are provided with a secure and simple solution in regard to scanning for politically exposed or high-risk individuals, as well as checking names against sanction, regulatory, law enforcement, and other official lists.

Use our sophisticated scan filters and due diligence workflow to minimise the amount of time you spend sorting through, false matches. Scan results and reporting sections allow you to access customer details, whenever and wherever required, as well as download reports, to customise for further investigation or to provide evidence of your AML program compliance for auditing purposes.

* This page is intended as general information only and should not be relied on as the sole source of information for your AML obligations and AML program. Please visit your local regulatory authority sites for the latest relevant and full information.