Nepal Rashtra Bank (Central Bank of Nepal) was established in 1956 to formulate and manage the requisite monetary and foreign exchange policies, preserving the banking and financial sectors’ stability and to develop a financial system, which is secure, healthy and efficient.

Securities Board of Nepal was established in 1993 as an apex regulator of the securities market to put in place the requisite securities regulations and directives, and take the necessary steps to avoid insider trading and crimes involving the securities market, and to supervise and regulate matters involving securities.

Financial Information Unit (FIU- Nepal) was established in 2008 as an Independent unit within Nepal Rashtra Bank. FIU is national agency entrusted with receiving, processing, analysing and disseminating financial information and data on suspected/potential money laundering and terrorism financing activities to law enforcement agencies and foreign FUIs.

As a designated service provider, you must ensure that you have a rigorous anti-money laundering/counter-terrorism financing policy in place, which includes the following:

Establish consistent procedures for CDD, risk profiling, and monitoring to ensure successful implementation of AML/CFT measures

Implement proper management oversight, supervision, processes, controls, segregation of duties, and training

Determine and confirm the identity of ultimate beneficial owners, and also update your framework on a regular basis, and keep a list of high-ranking officials and politically exposed persons

Each registered entity should consider the unique nature of its market, corporate structure, clients and transaction types, and other factors when adopting initiatives and procedures to ensure their effectiveness.

By devising sound legal and institutional structures, organising incremental capacity building activities, and raising awareness among stakeholders and the general public, Nepal has made significant progress in layering the groundwork for the AML/CFT system.

All AML/CFT programs must be risk-based. The risk assessment serves as the foundation for your entire anti-money laundering/counter-terrorism financing program. Your program must demonstrate clearly the connections between defined risks and the processes, practises, and controls that address those risks.

As a designated service provider, the company is required to notify FIU-Nepal regarding any suspicious activities. Notable ongoing reporting responsibilities are as follows:

- Banks and financial institutions: deposit or withdrawal of more than Rs 1 Million

- Real estate businesses: purchase or sale of a property for Rs 10 million or more

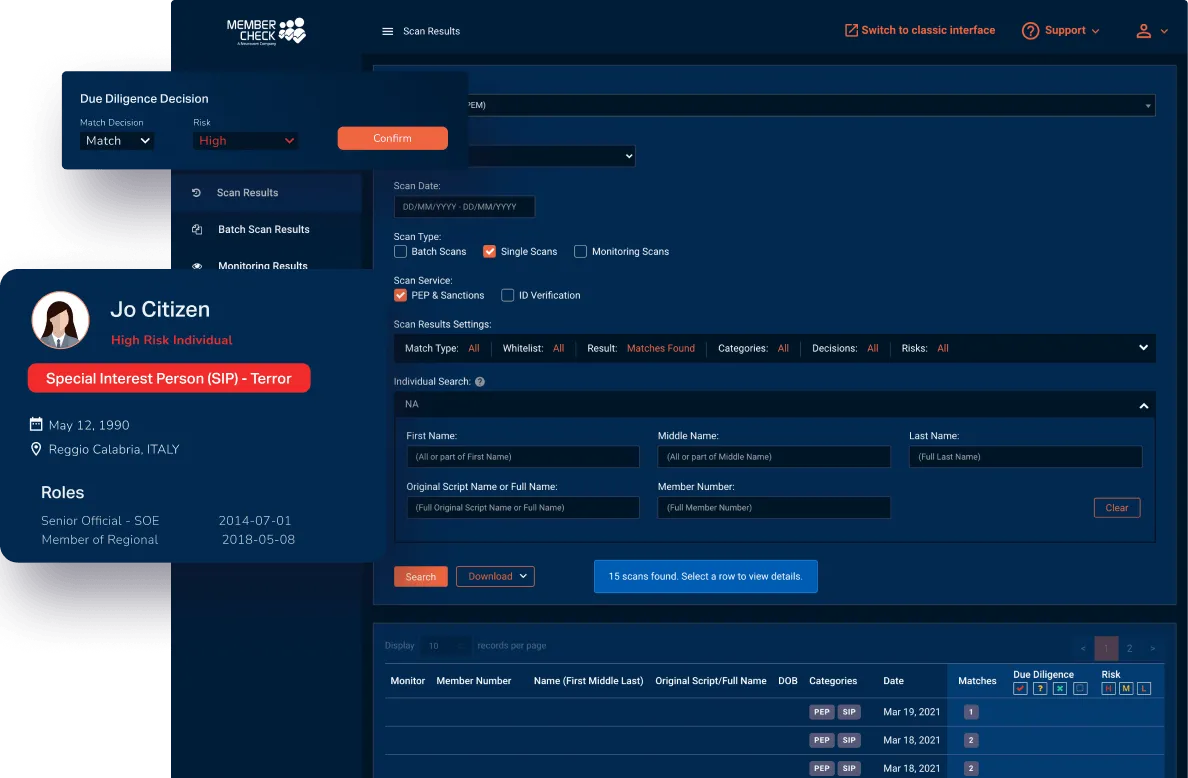

Our clients are provided with a secure and simple solution in regard to scanning for politically exposed or high-risk individuals, as well as checking names against sanction, regulatory, law enforcement, and other official lists.

Use our sophisticated scan filters and due diligence workflow to minimise the amount of time you spend sorting through, false matches. Scan results and reporting sections allow you to access customer details, whenever and wherever required, as well as download reports, to customise for further investigation or to provide evidence of your AML program compliance for auditing purposes.

* This page is intended as general information only and should not be relied on as the sole source of information for your AML obligations and AML program. Please visit your local regulatory authority sites for the latest relevant and full information.