AML/CFT Supervisors in Egypt

The Money Laundering Combating Unit (MLCU)

Apart from the international anti-money laundering policy, the Egyptian government has developed a domestic AML policy. In 2002, theEgyptian government enacted the Anti-Money Laundering Law (CML) to legally combat financial crime. This law makes money laundering a crime in Egypt. This law was strengthened in subsequent years by new AML regulations. The MoneyLaundering Combating Unit (MLCU) was established in 2002 under the CML Act. TheMoney Laundering Combating Unit (MLCU) is Egypt's financial intelligence agency.Anti-money laundering agencies are responsible for investigating suspicious transaction reports from financial institutions or other organizations. If a crime in a suspicious activity is discovered, then it to law enforcement.

Financial Regulatory Authority (FRA)

The Egyptian government established the Financial Regulatory Authority (FRA) in 2009 to begin auditing and regulating non-bank financial institutions. Financial regulators aim to ensure the development and stability of non-bank financial institutions. In addition, financial regulators take precautions to ensure that the non-banking financial industry is protected from financial crime.

The Supervisory Authorities are the Bangko Sentral ng [SS1] Pilipinas, the Securities and Exchange Commission, the Insurance Commission, or other government agencies designated by law to supervise or regulate a particular financial institution or Designated Non-Financial Business and Profession.

How to comply with the Money Laundering Combating Unit Egypt?

The objective of meeting MLCU requirements is to ensure that the Egyptian legal system meets international standards. Compliance program requirements include:

Onboarding Principles.

Principles of Customer Due Diligence.

Suspicious transaction reporting procedures.

Principles of documentation and retention and transmission of information.

Need for independent verification.

Notification to the Egyptian FIU, i.e. the MLCU.

The regulation requires certain parties, especially financial institutions, to conduct customer due diligence on customers with whom they have business relationships, report suspicious transactions related to money laundering and terrorist financing to MLCU, and request You must retain and submit the relevant information and documentation provided to you.

What are my AML/CTF reporting obligations?

- MLCU must be notified of all suspicious transactions regardless of their value. The term "transaction" need not refer to a single transaction, but may refer to multiple transactions.

- If multiple suspicious transactions are evaluated together, a single Suspicious Activity Report (STR) form must be completed.

- 'Information', 'Suspicion' or 'Reasonable Doubt' is sufficient to report a suspicious transaction.

- A Board-appointed “Compliance Officer” is responsible for reporting suspicious transactions to her MLCU.

- Suspicious transactions should be reported to MLCU immediately if in doubt. We take into account the time required for whistleblowing.

- Finding "information" about a transaction or customer associated with a suspicious activity report in the media or similar sources is clearly a situation requiring the submission of a suspicious activity report.

- Except for auditors tasked with duty during court proceedings and oversight of courts, suspicious transaction reports and related internal reports may not be explained to anyone, including the parties to the transaction.

- Do not refer to MLCU as a reference when conducting transactions to avoid misleading customers. MLCU does not have the authority or ability to approve or cancel transactions under applicable law.

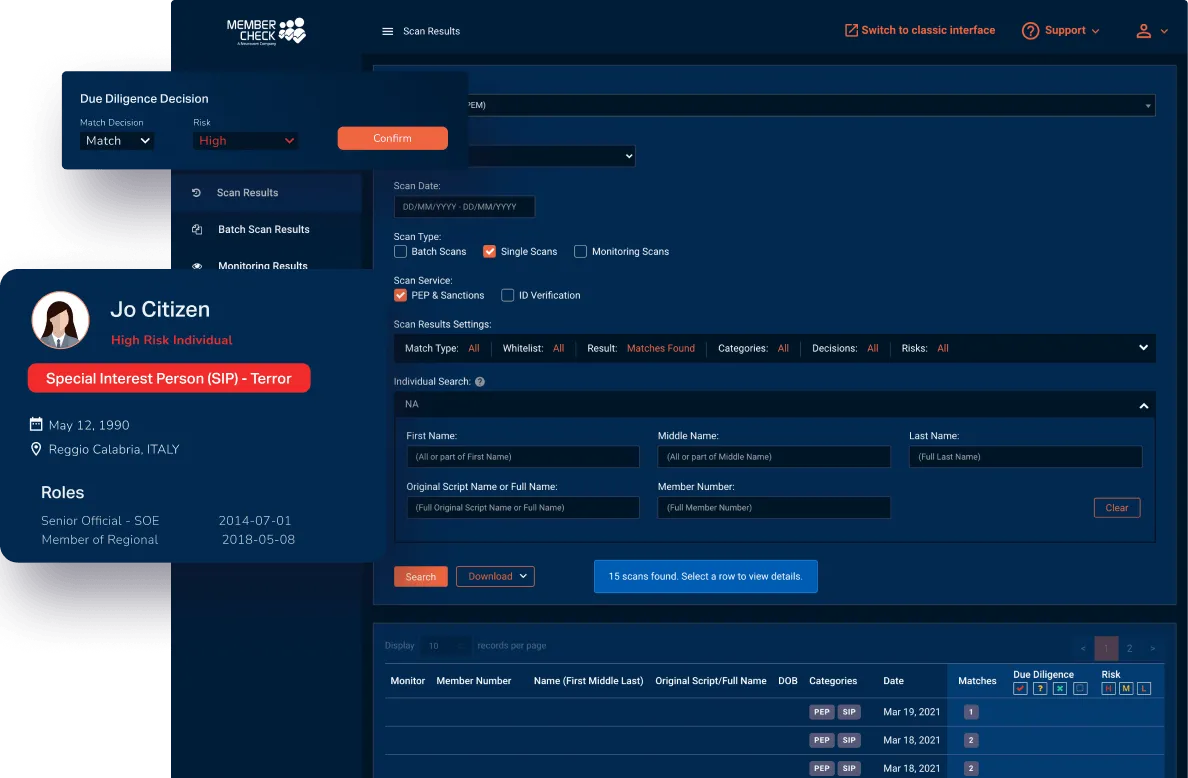

How can MemberCheck Help?

Our clients are provided with a secure and simple solution in regard to scanning for politically exposed or high-risk individuals, as well as checking names against sanction, regulatory, law enforcement, and other official lists.

Use our sophisticated scan filters and due diligence workflow to minimise the amount of time you spend sorting through, false matches. Scan results and reporting sections allow you to access customer details, whenever and wherever required, as well as download reports, to customise for further investigation or to provide evidence of your AML program compliance for auditing purposes.

* This page is intended as general information only and should not be relied on as the sole source of information for your AML obligations and AML program. Please visit your local regulatory authority sites for the latest relevant and full information.