State Bank of Pakistan (SBP) is the country's central bank, founded under the State Bank of Pakistan Act, 1956. The SBP Act requires the Bank to oversee Pakistan's monetary and credit systems. State Bank of Pakistan is the regulator for AML controls for Banks and related services. The Anti-Money Laundering, Counter-Terrorism Financing, and Counter-Proliferation Financing (AML/ CFT/ CPF) Regulations for SBP’s regulated entities were issued by SBP.

Securities and Exchange Commission of Pakistan (SECP) was operational on Jan 1, 1999, with the aim of developing a modern and efficient corporate sector, insurance, NBFCs and capital markets. SECP is in charge of ensuring that stockbrokers, commodity brokers, NBFCs, insurers, corporations, and non-profit organisations comply with AML/CFT regulations.

Financial Information Unit (FIU- Pakistan), established in October 2007, is Pakistan's central agency responsible of receiving, analysing, and disseminating financial information about suspected proceeds of crime and potential money laundering offences, as well as the funding of any operations or transactions linked to terrorism, to investigatory and supervisory authorities.

As a designated service provider, you must ensure that you have a rigorous anti-money laundering/counter-terrorism financing policy in place, which includes the following:

Conduct customer due diligence in compliance with their market and operating model, the nature and types of customers they serve, products they offer, and risk raised by their geographic location

Entities must determine the beneficial owners and take appropriate measures to verify their identity by using accurate and reliable documents, records, or information sources

All customer business relationships must be monitored on a regular basis to ensure that transactions are consistent and CDD is up to date

Implement appropriate internal policies and procedures for politically exposed persons, as well as ensure compliance with relevant record-keeping requirements including retention periods

Reporting entities must establish AML/CFT/CPF polices, processes, controls, responsibilities, and preventive measures that take into consideration their scale, nature of business, and operational complexities

Internal Risk Assessment Reports (IRAR) for assessing the effectiveness of existing AML/CFT policies, controls, obligations and preventive measures including STR/CTR

Each registered entity should consider the unique nature of its market, corporate structure, clients and transaction types, and other factors when adopting initiatives and procedures to ensure their effectiveness. IRAR is responsible for identifying, assessing, and comprehending ML/ TF/ PF risks at the entity level for consumers, products, facilities, distribution platforms, technologies, and employees etc.

All AML/CFT programs must be risk-based. The risk assessment serves as the foundation for your entire anti-money laundering/counter-terrorism financing program. Your program must demonstrate clearly the connections between defined risks and the processes, practises, and controls that address those risks.

As a designated service provider, the company is required to notify FIU-Pakistan regarding suspicious activity. Notable ongoing reporting responsibilities are the following:

There is no STR reporting threshold, and STR reporting is undertaken on any suspicious transaction, whether completed or attempted, regardless of the threshold. Reporting entities are required to maintain all the records related to STRs for a period of at least 10 years.

When a cash transaction exceeds a given threshold, which in this case is PKR 2 million or equivalent, a reporting agency is required to report it.

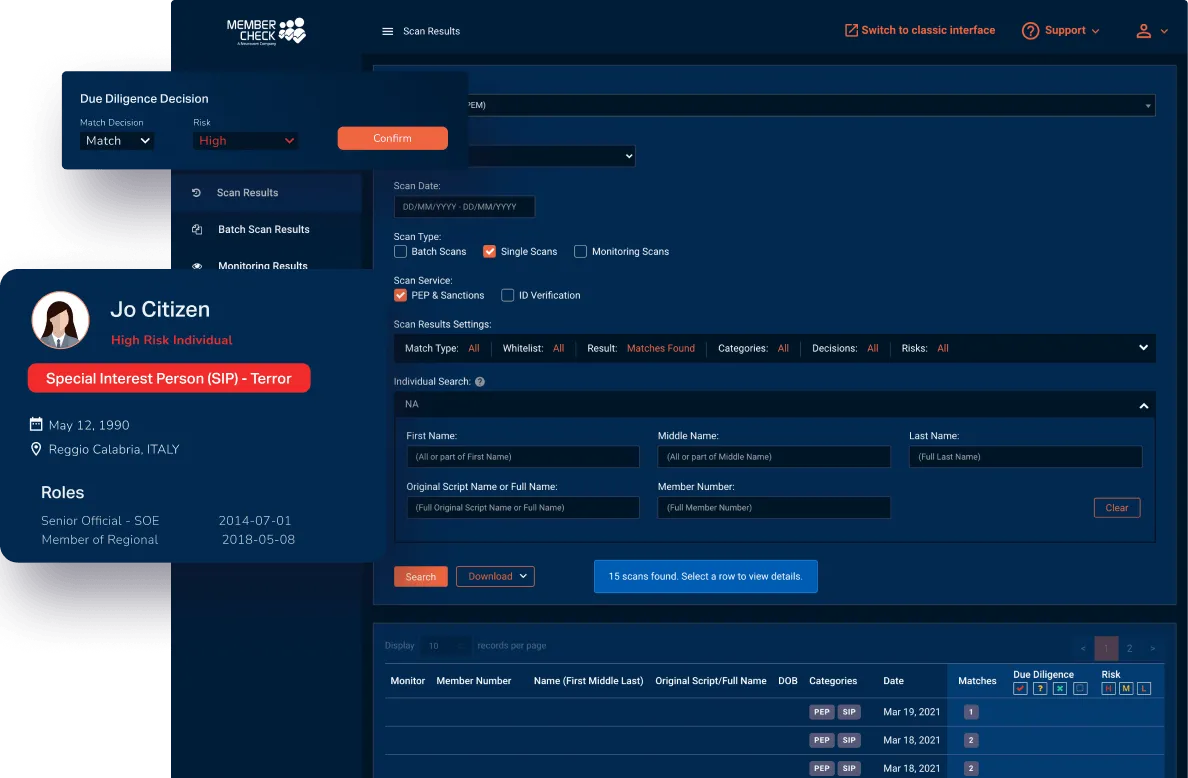

Our clients are provided with a secure and simple solution in regard to scanning for politically exposed or high-risk individuals, as well as checking names against sanction, regulatory, law enforcement, and other official lists.

Use our sophisticated scan filters and due diligence workflow to minimise the amount of time you spend sorting through, false matches. Scan results and reporting sections allow you to access customer details, whenever and wherever required, as well as download reports, to customise for further investigation or to provide evidence of your AML program compliance for auditing purposes.

* This page is intended as general information only and should not be relied on as the sole source of information for your AML obligations and AML program. Please visit your local regulatory authority sites for the latest relevant and full information.