The Da Afghanistan Bank is Afghanistan's central bank, responsible for licencing, regulating, and supervising banks, foreign exchange brokers, money service providers, payment system operators, securities service providers, and securities transfer system operators.

Afghanistan's Financial Transactions and Reports Analysis Center (FinTRACA) was formed in 2006 as a Financial Intelligence Unit (FIU) pursuant to the AML legislation. It has complete control in deciding how to collect, analyse, and disseminate knowledge about money laundering and terrorism financing. FinTRACA, in collaboration with financial regulators, law enforcement agents, and lawyers, leads to the establishment and maintenance of an atmosphere conducive to detecting and combating money laundering and terrorist financing in Afghanistan.

Each reporting entity is distinct and poses unique money laundering and terrorism financing threats. A financial institution's anti-money laundering policy should be proportionate to the scale, scope, risks, and sophistication of its activities, and should be adopted by the bank's or financial institution's board of directors, and be applicable to both domestic and international branches, as well as majority-owned subsidiaries.

All AML/CFT programs must be risk-based. The risk assessment serves are the foundation for your entire anti-money laundering/counter-terrorism financing program. Financial companies should have processes in place to classify, evaluate, track, handle, and minimise threats associated with money laundering and terrorism funding.

Financial institutions are required to have adequate policies, procedures and controls to combat potential money laundering and terrorism financing risk

You are required to identify customers properly

You must audit your AML/CFT program (as well as your risk assessment) every two years, or at any time as requested by your AML/CFT supervisor. A copy of your audit may be requested by your supervisor. Financial institutions are required to submit reports to FINTRACA for large cash transactions and suspicious transactions

Financial institutions are required to retain records of transactions

You are required to have staff that have been trained sufficiently to carry out their duties under this regulation

As a financial service provider, you must report certain transactions and suspicious matters to FinTRACA. Notable ongoing reporting obligations include:

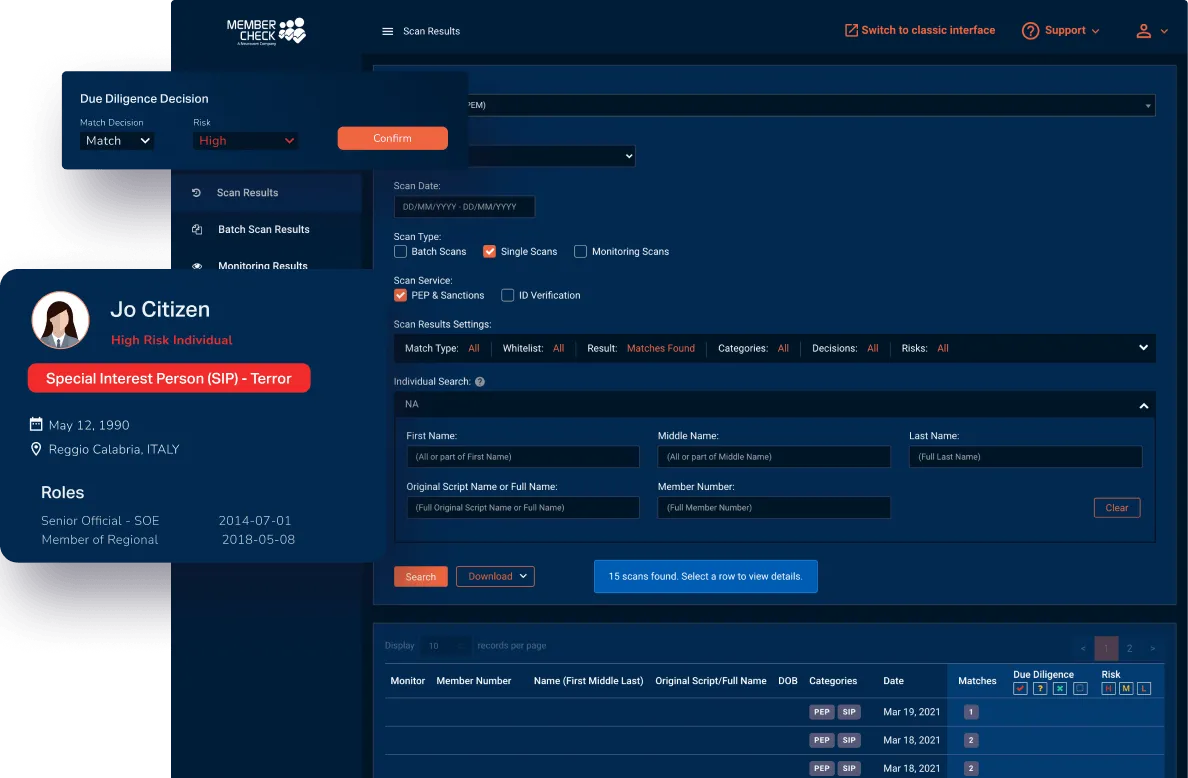

Our clients are provided with a secure and simple solution in regard to scanning for politically exposed or high-risk individuals, as well as checking names against sanction, regulatory, law enforcement, and other official lists.

Use our sophisticated scan filters and due diligence workflow to minimise the amount of time you spend sorting through, false matches. Scan results and reporting sections allow you to access customer details, whenever and wherever required, as well as download reports, to customise for further investigation or to provide evidence of your AML program compliance for auditing purposes.

* This page is intended as general information only and should not be relied on as the sole source of information for your AML obligations and AML program. Please visit your local regulatory authority sites for the latest relevant and full information.